As a mission-based cooperative lender and member of the Farm Credit System, CoBank is committed to serving as a good corporate citizen. The bank maintains a variety of corporate social responsibility programs primarily focused on rural America and the vitality of rural communities and industries.

We deliver vital support for the U.S. rural economy, providing financial services to agribusinesses and rural power, water and communications providers in all 50 states. It's who we are and what we believe in. Join us.

The U.S. harvested the second-biggest corn and soybean crop on record this fall, improving carries in the futures market and lifting the margin outlook for grain elevators storing corn and soybeans.

The dry harvest conditions this fall lowered the moisture content of both the corn and soybean crops, improving storability of the crops but costing grain elevators drying revenue.

Feed usage remains robust for both corn and soybeans with steady numbers of beef cattle on feed, hogs, pigs and chick placements.

Biofuel demand for corn and soybeans has experienced tremendous growth but faces headwinds from weakening profit margins and policy uncertainty going into the next administration.

Export demand has been robust for corn and soybeans, but a strong dollar, potential record-large corn and soybean crops in South America and volatile trade policy could cloud the export outlook.

Introduction

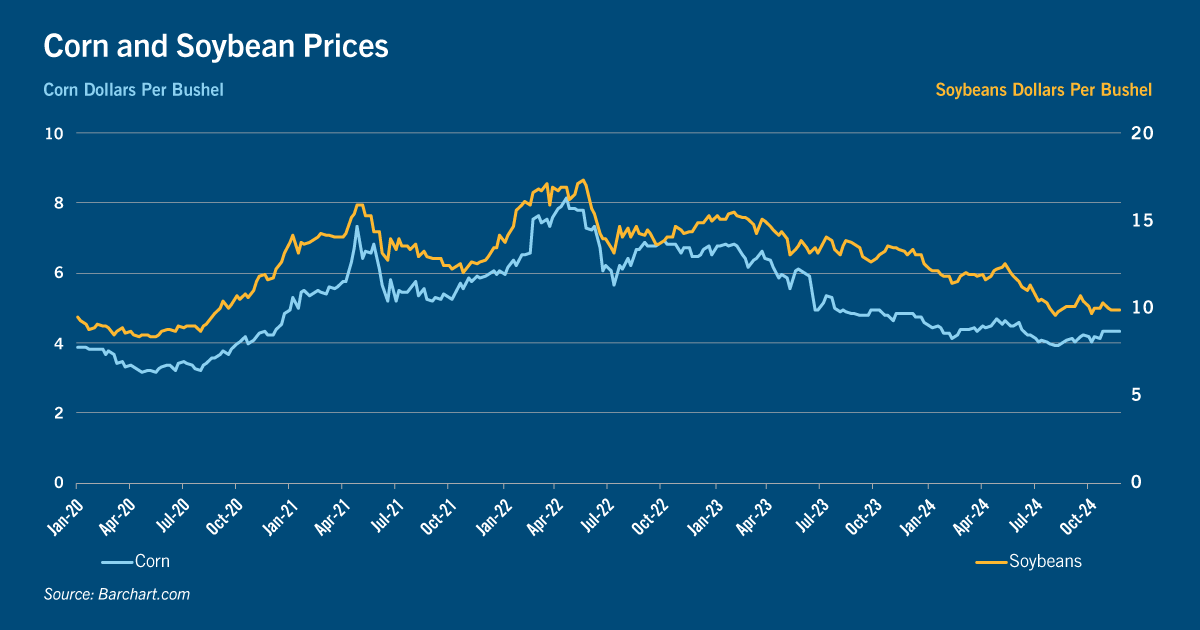

U.S. farmers harvested the second-biggest corn and soybean crops on record this fall with USDA estimating the U.S. corn crop at 15.14 billion bushels, down 1.3% from last year’s record crop, and the soybean crop at 4.46 billion bushels, up 7.2% YoY. Prices of both commodities have fallen to four-year lows, spurring additional demand both domestically and on the export front.

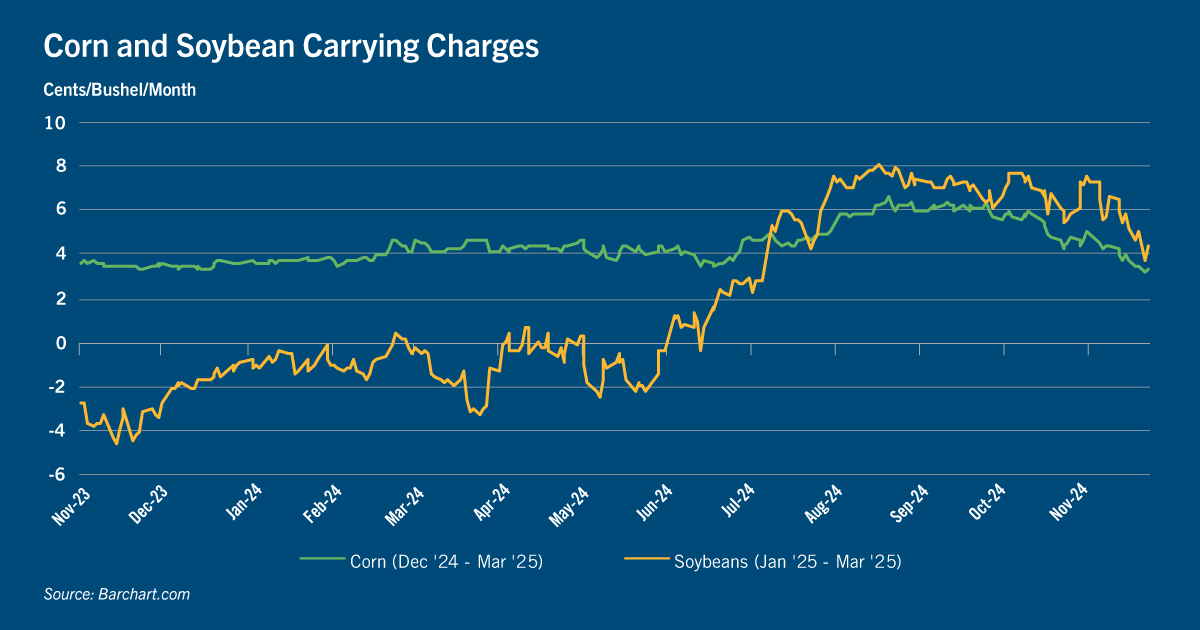

Strong domestic demand, driven by the acceleration in biofuel demand and a robust export program, have helped clear the abundant corn and soybean inventories in the U.S., which have narrowed the futures carries for both commodities. Carries occur when there is a surplus of a commodity, causing the price of deferred futures contracts to rise above nearby contracts, thereby incentivizing storage.

Feed demand also remains a bright spot for both corn and soybeans. Feed usage is expected to remain robust with steady numbers of cattle on feed in the beef sector, as well as hogs, pigs and chick placements. Demand for feed should hold consistent on the dairy front as herd inventory levels are stable.

The exhaustive usage pace, both domestically and on the export front, face growing headwinds. The U.S. dollar is expected to continue strengthening in a growing U.S. economy. However, trade disruptions with key trading partners China and Mexico could create harmful and lasting impacts to U.S. exports. Additionally, uncertainty in the biofuel policy raises uncertainty over the durability of domestic demand for corn-based ethanol and soybeans used for biodiesel and renewable diesel. The expectation for record corn and soybean crops in South America further cloud the demand outlook for U.S. corn and soybeans. The potential slowdown in both exports and domestic demand amid supply abundance improves the profit outlook for storage via a weakening of buy basis in the cash market and a widening of futures spreads in both corn and soybeans.

Corn

With ample carryover stocks from last year’s record harvest on top of this year’s large harvest, corn inventories in the U.S. are bulging. The stocks-to-use ratio for this year’s corn balance sheet is figured at 12.9% based on USDA’s latest projections, up from 11.8% last year. Corn piles are evident across the countryside due to lack of storage space. Elevators note that moisture levels of this year’s corn harvest are well below normal, reducing the risk of shrink. The low moisture content implies a low-margin year in drying revenue at grain elevators.

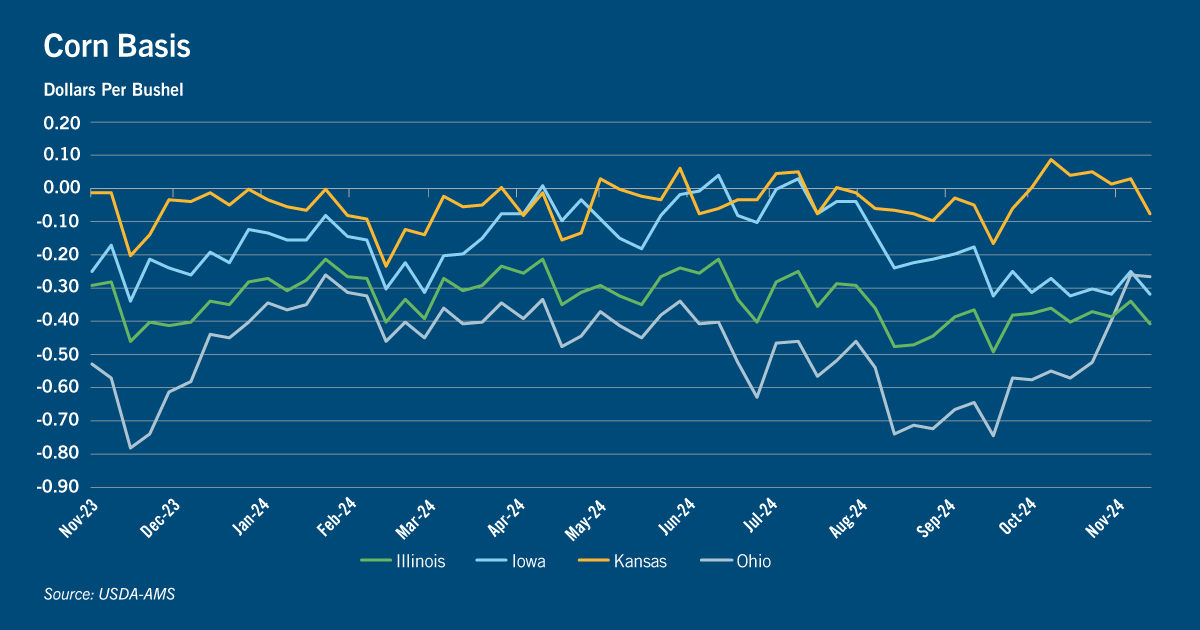

Corn has enjoyed an impressive demand story with a trifecta of strong ethanol, livestock and export demand amid slow farmer sales lifting corn basis higher nationwide. The strong demand on corn has also narrowed spreads in the futures market in recent weeks, eroding the profit incentive for storage.

Demand risk is of concern in the weeks ahead. While basis in the Corn Belt has been driven higher by record-strong ethanol demand, ethanol margins are turning negative amid tightening corn basis, rising natural gas prices and softening fuel prices, portending a slowdown in ethanol demand in the months ahead. There is considerable uncertainty in biofuel policy with the ongoing delay in releasing details on the 45Z clean fuel tax credit and the potential risk of increased small refinery exemptions from the Renewable Fuel Standards that were more common in the previous Trump administration.

The small refinery exemptions allow specific refineries from having to comply with the RVO (renewable volume obligation) targets. Each of these may curtail demand for corn ethanol during an already difficult time for this industry.

Export demand has been impressive and is putting more upward pressure on basis. Total U.S. corn export commitments are up 39% YoY with Mexico alone comprising 41% of all U.S. export sales. Demand from most foreign customers has also improved since last year, stimulated by low corn prices. This could also be attributed to expected trade disruptions that may occur going into the next administration. Mexico’s unshipped corn purchases total 8.2 million metric tons, up 4% YoY, with some purchases at risk of cancellation if retaliatory measures against the U.S. go into effect.

Replacing U.S. corn will be difficult for Mexico with livestock operations located in the northern region of the country, making the ease and efficiency of rail shipments from the U.S. hard to immediately replace. Imports from other corn exporters like Argentina or Brazil would be sent by ocean vessels to the coast, then unloaded onto rail to be shipped inland.

South America’s corn crop is also expected to be larger this marketing year, which when harvested, will bring new export problems for the U.S. Assuming normal growing conditions, USDA forecasts Brazil’s corn crop at 127 MMT, up 4.1% YoY, and Argentina’s crop up 2% YoY at 51 MMT, with both countries expected to be more competitive on the export front.

Amid the speculation regarding trade and biofuel policy, U.S. feed demand is expected to remain a consistent and positive driver of corn demand. With consistent cattle placements on the Plains, basis across the region is expected to remain comparatively strong.

Soybeans

The large U.S. soybean harvest and carryover stocks from the previous crop have left the U.S. with record soybean supplies. USDA forecasts the U.S. soybean stocks-to-use ratio to climb to 10.8% this marketing year, well above last year’s 8.3%.

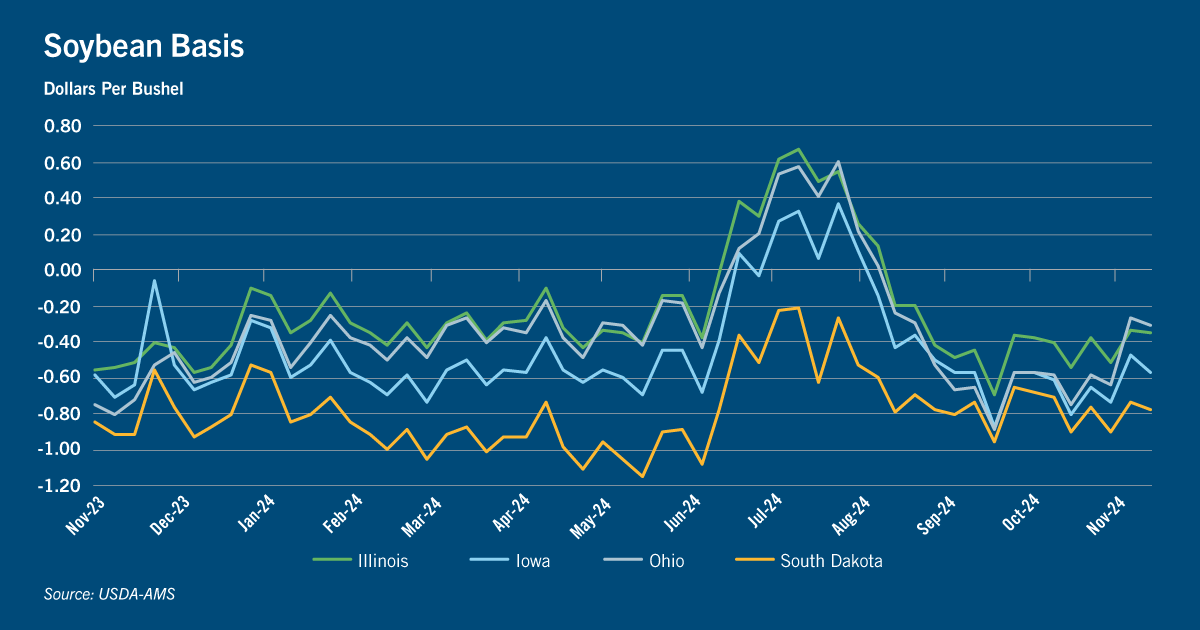

Soybean basis has strengthened in recent weeks while futures spreads have narrowed on the combination of a swifter export pace and persistent growth in U.S. crush demand. Domestic demand is robust, with soybean crush capacity still expanding to feed the rising demand of renewable diesel in the U.S., driven largely by California’s Low Carbon Fuel Standard. New soybean crush capacity and expansions are slated to come online in the months ahead. Growth is maturing as profit margins in the production of renewable diesel erodes, largely because of falling prices of renewable identification numbers (RINs).

On the export front, total U.S. export commitments for the current marketing year are up 9.0% YoY while Chinese purchases are down 8.5% YoY. Faster sales into other export markets like the European Union, Egypt and Southeast Asia have made up for the loss in Chinese demand so far this year. Soybeans have the most at risk in a trade dispute with China, which accounts for 46.7% of all U.S. soybean export commitments this year. China currently has 4.2 MMT (154.3 million bushels) of unshipped soybeans already purchased from the U.S., comprising 38.6% of all unshipped bushels to all export destinations that are still on the books. Concern is growing that unshipped soybean sales to China are at risk if a trade dispute arises.

Trade issues will create increased economic uncertainty for the U.S. at a time when South America is expected to harvest a record soybean crop in 2025. USDA currently figures the Brazilian soybean crop at 169.0 MMT, up 10.5% YoY, and the Argentine crop at 51 MMT, up 5.8% YoY. A trade dispute with China is widely expected to cause a shift in its soybean purchases to South America, which bring its harvest to market by late February to early March. As the new administration begins in January, China has begun to stockpile soybeans in anticipation of trade uncertainty.

However, not all aspects of renegotiating trade agreements and executing enforcement with China would necessarily be bad for soybeans. Tariffs on imports of used cooking oil (UCO) from China would incentivize use of domestic soyoil and could potentially accelerate the U.S. soybean crush pace. UCO is a major feedstock in the production of renewable diesel, according to the U.S. Energy Information Administration.

Outlook

The export outlook for corn and soybeans is most at risk in the months ahead. The combination of excess corn and soybean supply in the U.S., record crops from South America, potential retaliatory tariffs and cancelations of export sales will cause a sudden drag on exports. U.S. corn and soybean exports would be rerouted, slowing the overall export pace and increasing the cost of shipping into smaller markets. In a supply-surplus environment, the higher transportation cost will be borne by the farmer via wider basis.

The value of the U.S. dollar could also continue strengthening, creating additional headwinds for corn and soybean exports. Additional tax cuts and increased deficit spending being considered by the incoming administration would push the dollar higher. As in any new administration, changing geopolitics could cause changes to the dollar, further underpinning its value. The robust export pace for corn and soybeans is likely to fade after Jan. 1.

The weakening margin outlook for biofuels and the heightened policy risk for all biofuels under the second Trump administration risks slowing ethanol demand for corn and crush demand for soybeans. A robust livestock sector signals continued strength in feed demand, although not enough to absorb potential losses in exports.

The combination of growing world supplies and slowing export pace in 2025 will incentivize storage of both corn and soybeans, with elevators benefiting from bigger carries in the futures market.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.

Stay ahead of the game in your field. Subscribe today.

Get CoBank's industry-leading Knowledge Exchange research reports delivered straight to your inbox as soon as they're released.

Have a comment or question about these reports?

Contact CoBank's Knowledge Exchange team to ask questions, engage with analysts or receive additional information.